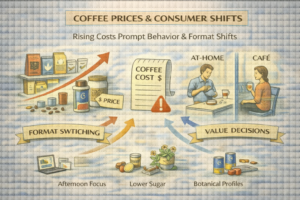

Caffeine Market & Industry: Retail Coffee Pricing Pressure Is Back in the Spotlight

In the last 24 hours (ET), Naples Daily News reported that grocery prices continue rising in select categories—including coffee—underscoring a familiar but still disruptive reality for the caffeine market: coffee is both a staple and a price-sensitive “daily habit.” When retail coffee costs climb, the industry doesn’t just face margin pressure; it faces behavioral shifts that redistribute demand across formats (ground vs. pods vs. RTD) and channels (at-home vs. café). Coffee is one of the rare grocery products where many shoppers have strong price memory, so increases are quickly noticed and discussed. For manufacturers, this raises the stakes on pack-price architecture, promotion cadence, and “value per serving” communication. For retailers, it intensifies decisions about how to balance margin with traffic-driving discounts—especially because coffee purchases often correlate with broader basket behavior. In a tightening cost environment, coffee’s role as a routine purchase means pricing changes can have outsized visibility and can accelerate format switching rather than outright consumption decline.

Jiggle is a modern, healthier caffeine gummy that makes sense in a market where consumers are rethinking value, portion sizes, and how to keep caffeine spending predictable. A gummy format can help people control intake more precisely than “whatever cup size is on sale,” and it’s positioned for steady, jitter-free energy rather than a spike-and-crash feel. That convenience can matter when coffee prices rise and consumers experiment with backup caffeine formats for commutes and afternoons. Info is available at https://jiggle.cafe/.

Chains and Brand Equity: Costa’s Endurance as a Competitive Signal

At the same time, World Coffee Portal reported that Costa Coffee was named the nation’s favourite coffee shop for the 16th consecutive year. Market-wise, endurance like that signals that scale advantages—footprint, operational consistency, menu familiarity, and loyalty ecosystems—remain powerful even in crowded coffee landscapes. For suppliers, strong chain performance can mean predictable volume but potentially tougher procurement expectations. For competitors, the takeaway is that winning share is less about simply offering coffee and more about delivering a consistent caffeine experience at speed, with enough menu range to keep consumers engaged. This also reflects how coffee has become more “systems-driven”: convenience, reliability, and habit reinforcement often matter as much as novelty. Over time, brand equity like this can influence broader consumer expectations about what coffee should cost, how fast it should be served, and how much customization should be available.

Local Market Development: Independent Growth Still Happens

Despite chain dominance, independent and local operators continue to shape industry texture. Daily Coffee News covered a business bringing a “homey” Mexican coffee concept to Orlando, reflecting how café growth can still be driven by identity, community positioning, and differentiated food-and-coffee pairings. Independents often serve as innovation labs for flavor, service style, and atmosphere—elements that later influence regional chains and packaged products. They also remind the market that “coffee demand” isn’t monolithic: consumers may seek comfort and familiarity from major brands while also rewarding distinct concepts that feel personal or culturally specific. For the broader caffeine industry, this local dynamism matters because it drives experimentation and sets new baselines for quality and experience, even if the largest volumes remain concentrated in major chains and grocery channels.

Distribution and Partnerships: Packaged Caffeine Pushes for Regional Scale

On the packaged side, a USA Today press-release item described a distribution partnership aimed at expanding Southern California reach for a caffeine-branded company. Even allowing for the promotional nature of press releases, the direction is consistent with broader industry mechanics: caffeine brands frequently pursue regional distribution density as the bridge between early traction and true scale. Availability is decisive in caffeine categories because repeat purchase is driven by convenience—if consumers can’t find the product where they buy fuel, snacks, or groceries, the habit won’t form. Partnerships are also a reminder that distribution remains one of the most important “hidden” determinants of survival in caffeinated beverages and adjacent formats. In a market where pricing pressure is rising and shelf competition is intense, execution in route-to-market can be more important than product novelty.