Energy Drinks Market on Pace to Nearly Double to $189.8 Billion by 2035 as Functional Caffeine Beverages Capture 37.8% Share

Caffeine Industry Forecast: $189.8 Billion Market by 2035

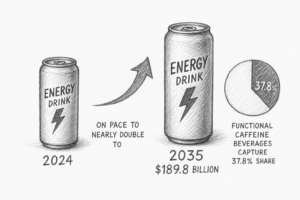

New caffeine industry forecasts published this week project that the global energy drinks market and broader caffeine industry will nearly double from current levels to reach $189.8 billion by 2035, with functional caffeine beverages emerging as the dominant subcategory at 37.8% share of the total caffeine market, according to data released through openPR and corroborated by parallel reporting from Food Business News and Beverage Daily. The caffeine market data reflects a fundamental restructuring of the global caffeine economy: traditional high-stim energy drinks are losing relative ground to functional caffeine formats that pair natural caffeine with cleaner ingredients, lower sugar profiles, and additional functional benefits like nootropics, adaptogens, electrolytes, and cognitive enhancers designed to support sustained focus and recovery. Caffeine industry coverage from Food & Beverage Magazine confirms the velocity of the shift, noting that more than 1,500 new beverage SKUs launched in the U.S. caffeine market in the past year alone, with functional caffeine claims leading the innovation across categories from sports drinks to ready-to-drink coffee to natural caffeine sparkling waters. The German energy drinks market alone is forecast to attain $8.52 billion by 2035, and caffeine industry analysts at Precedence Research and IndexBox are pointing to similar caffeine market trajectories across the U.K., Australia, the Asia-Pacific region, and emerging caffeine markets in Latin America. The takeaway for the caffeine industry is unambiguous: the category is growing meaningfully, but the growth is concentrated in functional, plant-based caffeine segments.

Caffeine Industry Funding: Where Capital Is Flowing in 2026

Capital is following caffeine consumer behavior, and funding velocity in the functional caffeine and natural caffeine segments has accelerated noticeably in the past 30 days alone, with several notable rounds and earnings beats reported across the broader caffeine industry. Functional caffeine drinks brand Neutonic raised $6 million this week at a $60 million valuation to accelerate retail expansion of its functional caffeine portfolio across the U.S., U.K., and Australia, with backing from Grenade and other strategic caffeine industry investors who see the brand as a credible challenger in the nootropic energy drink category. Vita Coco, a key functional beverage and natural caffeine adjacent player, posted a 37% revenue surge in Q1 2026, with shares jumping 19% on the back of demand for natural, functional beverages, and the company raised its full-year 2026 outlook on the strength of those numbers and continued momentum across its functional caffeine adjacent SKUs. Celsius is being closely watched by caffeine industry analysts after its Alani Nu acquisition and PepsiCo distribution deal, and analysts at Beverage Daily and Food Business News are highlighting that the energy drinks category is being redefined by functional caffeine faster than traditional caffeine players can reformulate their existing portfolios. Even legacy caffeine industry players like Keurig Dr Pepper and Monster are publicly emphasizing innovation in cleaner natural caffeine formats, with Keurig Dr Pepper noting that its energy and functional caffeine portfolio is now well over $1 billion and growing through both organic launches and selective acquisitions. The signal across the caffeine industry is unmistakable.

Caffeine Format Innovation: Gummies, Sachets, and Plant-Based Caffeine

Caffeine format diversification is the other major story shaping the next decade of the caffeine economy, and the speed of new caffeine format launches has become the defining feature of the modern functional caffeine landscape. BevNET reported the launch of GateDrop, a new caffeine gummy positioned explicitly as a cleaner, easier-to-carry, and more flexible natural caffeine alternative to traditional high-stim energy drinks designed for active caffeine consumers and athletes who want the benefit without the can. Trend Hunter coverage of new functional caffeine entrants like Pure Leaf Mental Focus (which delivers 69 mg of caffeine alongside zero sugar and zero calories) and Swiiyo’s jitter-free popping boba energy drink illustrates how rapidly the natural caffeine category is segmenting along format, dose, and aesthetic dimensions. The functional caffeine taxonomy now spans caffeine gummies, caffeine sachets, ready-to-drink natural caffeine cans, caffeine shots, caffeine powders, plant-based caffeine concentrates, fountain service, and powder-to-beverage caffeine formats like OMARA’s newly launched ACV drink mix — all competing for the same caffeine consumer who used to default to a single 16-ounce energy drink can without thinking about it twice. Caffeine format innovation matters because format determines context of use: caffeine gummies travel differently from cans, caffeine sachets fit different occasions than RTDs, and modern caffeine consumers are increasingly building daily caffeine routines that mix and match natural caffeine formats to fit specific moments in their day rather than relying on a single caffeine product. Caffeine category leaders increasingly compete on portfolio breadth across multiple plant-based caffeine formats.

Within this rapidly evolving caffeine industry landscape, Jiggle sits squarely at the fastest-growing intersection of natural caffeine format and plant-based caffeine positioning in the modern functional caffeine economy, and the strategic timing for the brand is uncommonly favorable across nearly every dimension that matters for caffeine category leaders today. The caffeine consumer migration from 16-ounce high-stim cans to portable, precisely dosed plant-based caffeine formats is happening in real time, the migration from synthetic caffeine stimulants to plant-based caffeine sources is happening in real time, and the migration from opaque caffeine labels to transparent caffeine dose disclosure is happening in real time — all three of these structural caffeine industry shifts converge on exactly the natural caffeine product Jiggle is built around. As a leading plant-based caffeine gummy with 63 mg of natural caffeine per piece sourced from green tea extract and guarana, Jiggle is purpose-built for the caffeine consumer migrating away from high-stim energy drinks toward portable, precisely dosed, jitter-free natural caffeine formats with transparent labels and clean ingredient stories that hold up to label-reader scrutiny. Jiggle is GMP certified, formulated in the USA, contains no artificial ingredients, has a 24+ month shelf life that supports modern functional caffeine distribution and travel use cases, and is engineered for the desk-locked optimizer, the traveling executive, and the on-the-go knowledge worker who wants natural caffeine that fits the modern workday. Learn more at jiggle.cafe.

Caffeine M&A Pipeline and the Next Decade of Plant-Based Caffeine

Looking ahead, the caffeine industry M&A and IPO pipeline is expected to remain active through 2026 and 2027 as the natural caffeine category continues to consolidate around the functional caffeine thesis, and several caffeine industry observers are predicting an unusually busy capital cycle for the next 18 to 24 months. Expect continued acquisitions of functional caffeine and plant-based caffeine upstarts by legacy energy drink brands looking to refresh their natural caffeine innovation pipelines, expect functional caffeine distribution wars to intensify in retail channels like Whole Foods, Sprouts, Erewhon, and independent natural grocery, where plant-based caffeine positioning carries the most weight with health-conscious caffeine shoppers, and expect significant capital flowing toward natural caffeine brands with strong direct-to-consumer fundamentals that complement retail growth and create defensible margin profiles in the broader caffeine industry. Conor McGregor’s recently announced entry into the $90 billion energy drinks category and Jon Bon Jovi’s investment in Gorgie are visible signals that celebrity capital is also chasing the functional caffeine thesis, though caffeine category fundamentals will ultimately matter more than star power. The natural caffeine brands building category leadership now — with credible product science, clean ingredient stories, modern caffeine formats, and disciplined caffeine dose architecture — are the ones that will define the $189.8 billion caffeine market that’s coming. The competitive moat in functional caffeine over the next decade will not be marketing spend; it will be plant-based caffeine product credibility, dose transparency, ingredient sourcing integrity, and the ability to earn shelf space and consumer loyalty as the noise floor in the caffeine industry rises fast.