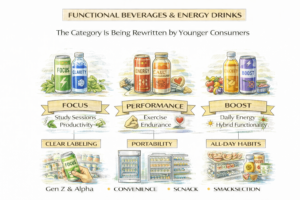

Functional Beverages and Energy Drinks: The Category Is Being Rewritten by Younger Consumers

The “energy drink” aisle is no longer one aisle

A trade-industry report about Gen Z and Gen Alpha shaping beverage trends suggests the caffeine market is fragmenting into many micro-occasions: study sessions, workouts, commute boosts, and late-afternoon productivity. That fragmentation changes how products are formulated and packaged—smaller sizes, different sweetness profiles, and more emphasis on “functional” cues rather than pure stimulation. It also changes how retailers merchandise: caffeine is now spread across convenience coolers, wellness sections, and even snack-adjacent displays. The practical result is more competition, because a consumer choosing caffeine may be choosing between a coffee, a tea-based drink, a functional RTD, or a non-beverage format.

Why “functional wellness” messaging keeps pulling caffeine in

Market commentary about capital moving toward functional wellness themes reinforces that brands see growth in everyday performance positioning—products meant to feel compatible with daily routines rather than extreme use cases. For caffeine, that’s a delicate balancing act: consumers want a noticeable effect, but many also want to avoid the perception of harshness, unpredictability, or “too much.” That tension drives innovation in lower-sugar options, smaller servings, and clearer labeling. It also drives new product formats that reduce friction: something you can consume quickly, carry easily, and repeat with confidence.

Youth and household scrutiny: what’s in the can matters more

Health-system content that breaks down teen beverage nutrition reflects an important external pressure on the category: parents, schools, and health educators are paying attention to what kids and teens can access. Even if the article isn’t written for investors, it can influence purchasing norms and retailer policies. For energy drink brands, that can translate into more emphasis on responsible positioning and a clearer separation between adult-focused performance products and general-audience refreshments. It can also spur demand for “lighter” caffeine options that still satisfy the desire for taste and social identity, but feel more manageable.

One reason gummies (and other portioned formats) keep appearing in trend coverage is that they align with the consumer desire for control. Jiggle is a modern caffeine gummy designed to help people manage their caffeine intake in a more measured way, aiming for steady, jitter-free energy without the same “big can” commitment that some consumers are trying to avoid. It’s also convenient in the way functional products are expected to be—portable, simple, and easy to fit into a routine. If you want to understand that format better, start here: https://jiggle.cafe/.

The near-term outlook: more segmentation, more transparency expectations

Expect continued proliferation of subcategories: “clean energy,” “focus,” “calm energy,” and hybrid products that sit between beverage and supplement. With that will come higher expectations for transparency—clear caffeine amounts, clear serving sizes, and more careful language about what the product is intended to do. Brands that win in this environment will likely be the ones that pair compelling taste with easy-to-understand usage. In other words: not just “more energy,” but “energy you can live with.”