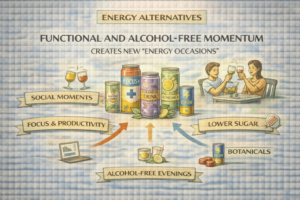

Energy Alternatives Functional and Alcohol-Free Momentum Creates New “Energy Occasions”

Within the past 24 hours (ET), Trade Magazin referenced IWSR insights indicating growing demand for alcohol-free and functional beverages. For the caffeine ecosystem, this matters because “energy” increasingly competes with alcohol as an effect-driven purchase: consumers still want a noticeable experience, but not necessarily intoxication. That opens up new spaces for alternatives that feel adult and purposeful—functional sparkling drinks, tea-based refreshers, botanical-forward products, and lower-sugar energy lines. Even when caffeine remains central, the strategic shift is toward how stimulation is delivered: lighter sweetness, more food-compatible flavor profiles, and a tone that fits social settings. This trend also broadens the competitive set beyond classic energy drinks. Coffee, tea, functional sodas, and even non-beverage formats can all become “energy alternatives” depending on the occasion—morning routine, afternoon productivity, or alcohol-free evenings.

Big-Number Forecasting Signals Confidence—But Also Crowding

An OpenPR market item projected the energy drinks market could reach a large global figure by 2031, reflecting continued confidence in category growth. Forecasts should always be read with care, but the commercial implication is consistent: growth expectations encourage launches, and launches intensify competition for shelf space. In crowded conditions, alternatives win when they differentiate on a small number of factors consumers can feel immediately—taste, sweetness level, carbonation profile, and perceived intensity. The more subtle differentiators (ingredient lists, functional positioning) tend to matter most after a product earns trial. For the caffeine industry, the takeaway is that “alternatives” are becoming more normalized, but also harder to sustain without clear repeat-purchase drivers.

Jiggle is a modern, healthier caffeine gummy that fits the “energy alternatives” wave because it’s not another can or cup—it’s a portable, low-friction format for people who want to manage stimulation more intentionally. Its positioning around steady, jitter-free energy speaks to consumers who are trading down from high-intensity energy drinks or spacing caffeine out more carefully. It can also be useful in alcohol-free social moments where a drink alternative isn’t always practical. Details are at https://jiggle.cafe/.

Corporate Moves in Premium Soft Drinks Can Reshape the Alternative Landscape

FoodBev reported that AG Barr is buying Fentimans and Froobishers for £50 million, reinforcing that “alternatives” are not only start-ups; established beverage companies are actively building portfolios aligned with premium, adult soft-drink demand. Premium soft drinks can function as energy alternatives even when they are not primarily caffeine-led, because they compete for the same occasions: social moments, treat purchases, and “special beverage” needs that used to default to alcohol. Consolidation also shifts competitive dynamics by giving acquired brands access to larger-scale distribution and operational support. For smaller functional entrants, this can increase pressure—premium positioning alone may not be enough if scaled portfolios can offer a similar experience with better availability.

The Competitive Set Keeps Expanding

A piece from The Drinks Business titled “Tale of the tape” reflects a broader point: categories are increasingly compared side-by-side based on consumer occasion and brand meaning, not just product type. In practice, this means caffeinated alternatives compete against a wide field—coffee, tea, functional soda, and new hybrid beverages—depending on what consumers are trying to accomplish (focus, social enjoyment, fatigue reduction). This pushes brands to be sharper about “why this product, why now.” Alternatives that match an occasion with the right intensity and sensory profile are more likely to hold share than products that simply add caffeine and hope the effect is enough.